From March 30th until April 1st , the European University hosted the fourth Workshop on Risk, Insurance and Finance, which is held every year by the Department of Economics. This year, the organizing committee invited professors from the University of Trieste, in Italy. Each professor gave several lectures: Ermanno Pitacco spoke about insurance and risk management, and Anna Rita Bacinello spoke about finance.

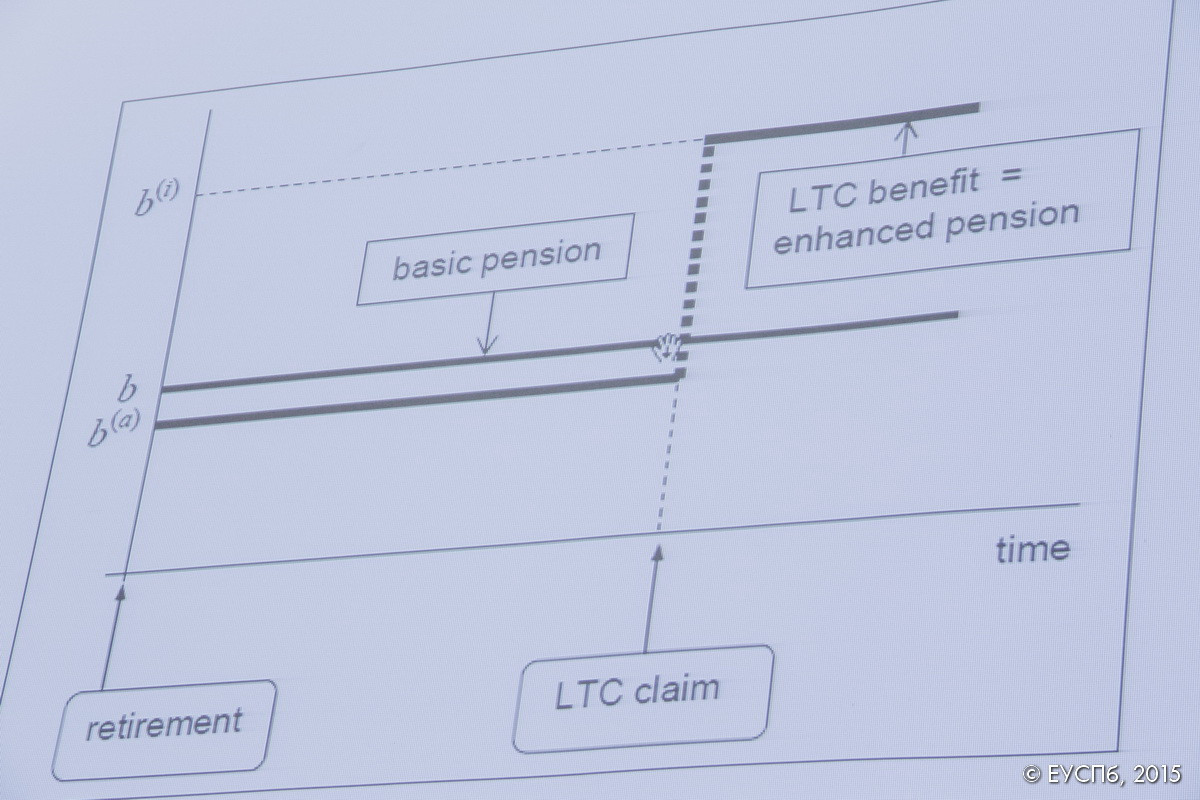

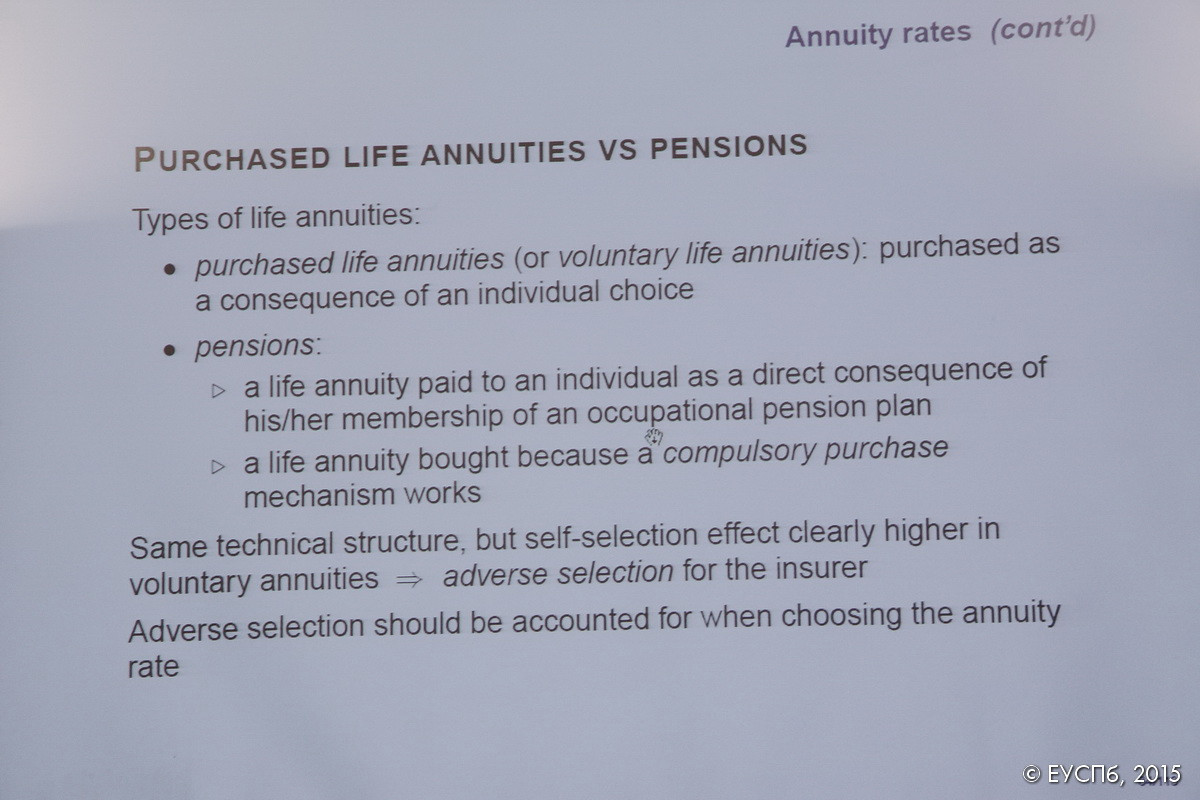

Ermanno Pitacco’s lecture on the first day reviewed various instruments used in forming post-retirement income. For natural reasons, every person after a certain age gradually loses the ability to work, but still requires income for the next years of life. There are diverse ways of solving this problem. These include government programs of mandatory retirement insurance, as well as voluntarily acquired financial products offered by private agents, such as a life annuity contract. Pitacco noted that the life annuity contract presents itself as an insurance and investment product. What are the principles underlying the decision to purchase such a product, how an insurance company decides its financial structure, as well as how the individual and collective risks involved are linked to the instrument of life annuity from the insurer’s point of view.

Aside from traditional risks, modern actuaries pay special attention to the issue of increasing life expectancy. It is unclear exactly what laws this change has been subject to in the last century, and how to predict its future value. Furthermore, the instability of financial markets as a whole causes volatility in using life annuity as a financial instrument (it becomes increasingly complex). Pitacco went on to describe a series of possible life annuity designs based on payment structure at the accumulation phase (a one-time payment, or account replenishment) and at the receipt of payments phase (a complete one-off at some point after retirement or multiple times at a certain frequency; the sum is either fixed or determined based on the number of survivors within an age cohort); he examined the pros and cons for both insurers and the insured. Pitacco mentioned that the European legal system, for example, forbids discrimination against consumers based on sex even though risks differ for men and women. In this regard, insurers must offer special conditions for all consumers.

On the second day, Pitacco devoted his lecture to annuities design. He listed several sources of risk—changing interest rates, adverse selection, increased life expectancy—focusing primarily on the latter. In the modern world, life expectancy is growing steadily (albeit with variable speed). As the modal value of life expectancy increases, mortality (survivorship) curves are becoming more prominent. For actuaries, it is especially important to precisely predict the behavior of mortality curves for the elderly and extremely elderly (since deviation of real life expectancy from the expected value can lead to non-diversifiable risk), even though such a prognosis presents a technically difficult task. Insurance companies conceptualize their own solvency models based on this, of which Pitacco presented several different versions.

On the third day of the workshop, Professor Anna Rita Bacinello gave a lecture on the evaluation of life insurance contracts. She presented Boyle, Brennan and Schwartz’s model as a basis, in which guaranteed payments are expressed in terms of European options. Hereafter, the model is consistently complicated in considering various types of options, guarantees, and combinations thereof. Additionally, to evaluate minimum guaranteed payments, static, mixed, and dynamic approaches are used for modeling policyholder behavior. Through qualitative examples, Bacinello demonstrated that the differences between various approaches of behavior at a low rate are significant.

Alena Skolkova